The VSME Standard simplifies ESG reporting for SMEs, helping businesses improve transparency, attract investment, and contribute to sustainability goals.

Maikel Fontein

5

min

The VSME (Voluntary Sustainability Reporting Standard for Micro-, Small-, and Medium-Sized Enterprises) offers a comprehensive framework for non-listed companies to report on sustainability issues in an accessible and proportional way. This voluntary standard, crafted by the European Financial Reporting Advisory Group (EFRAG), addresses the increasing demand for transparency from smaller enterprises regarding their environmental, social, and governance (ESG) performance. The aim is to provide SMEs with a structured and straightforward path to integrate ESG considerations into their operations. It also seeks to facilitate their involvement in the larger, global sustainability effort. Here’s an in-depth look at the VSME Standard, how it works, and why it matters for SMEs.

What is the VSME Standard?

The VSME Standard was developed to help non-listed, micro-, small-, and medium-sized enterprises (SMEs) meet the growing demand for sustainability data from a variety of stakeholders, including large companies, investors, and banks. SMEs are increasingly being asked to provide information about their ESG performance, but the complexity and volume of reporting can often be overwhelming, especially for smaller businesses. This is where the VSME Standard comes into play—it provides a voluntary, flexible, and scalable reporting framework tailored to the needs and capabilities of smaller businesses.

Key Objectives:

Provide Transparency: The standard allows SMEs to disclose their environmental, social, and governance impacts consistently and comparablcy, making them more transparent to external stakeholders like customers, suppliers, and investors.

Meet Data Requests from Larger Businesses: Large businesses, which are often under pressure to track and report on the sustainability performance of their suppliers, can rely on the VSME Standard to obtain the necessary data from smaller enterprises.

Access to Financing: With sustainability becoming an increasingly important consideration for banks and investors, SMEs can use the VSME Standard to meet investor criteria and improve their access to finance.

Improve Sustainability Management: SMEs are often unaware of the full extent of their environmental and social impacts. The VSME Standard helps them identify areas where they can improve, from energy use to waste management and workforce safety.

Support a Sustainable Economy: By encouraging SMEs to integrate sustainability into their operations, the VSME Standard contributes to a more sustainable and inclusive economy, benefiting individual companies and society.

Who Does the VSME Standard Apply To?

The VSME Standard is specifically designed for micro-, small-, and medium-sized enterprises (SMEs) that are not listed on a regulated market in the European Union. Despite not being subject to the same regulatory pressures as listed companies, these SMEs can adopt the standard to demonstrate their commitment to sustainability, improve stakeholder relationships, and prepare for potential future regulations. These businesses are typically outside the scope of more comprehensive regulations like the Corporate Sustainability Reporting Directive (CSRD), which applies to larger companies. However, the VSME Standard encourages SMEs to voluntarily adopt these reporting practices to stay ahead of future regulations and increase their sustainability efforts.

The categorization of these businesses follows the thresholds defined by the EU, which classify companies as:

Micro enterprises: Businesses that do not exceed two of the following thresholds:

€450,000 in balance sheet total

€900,000 in net turnover

10 employees on average during the financial year

Small enterprises: Businesses that do not exceed two of the following thresholds:

€5 million in balance sheet total

€10 million in net turnover

50 employees on average

Medium enterprises: Businesses that do not exceed two of the following thresholds:

€25 million in balance sheet total

€50 million in net turnover

250 employees on average

While micro-undertakings are encouraged to use the Basic Module of the standard, larger SMEs can benefit from the Comprehensive Module to provide more detailed reporting on their sustainability practices.

Understanding the Structure of the VSME Standard

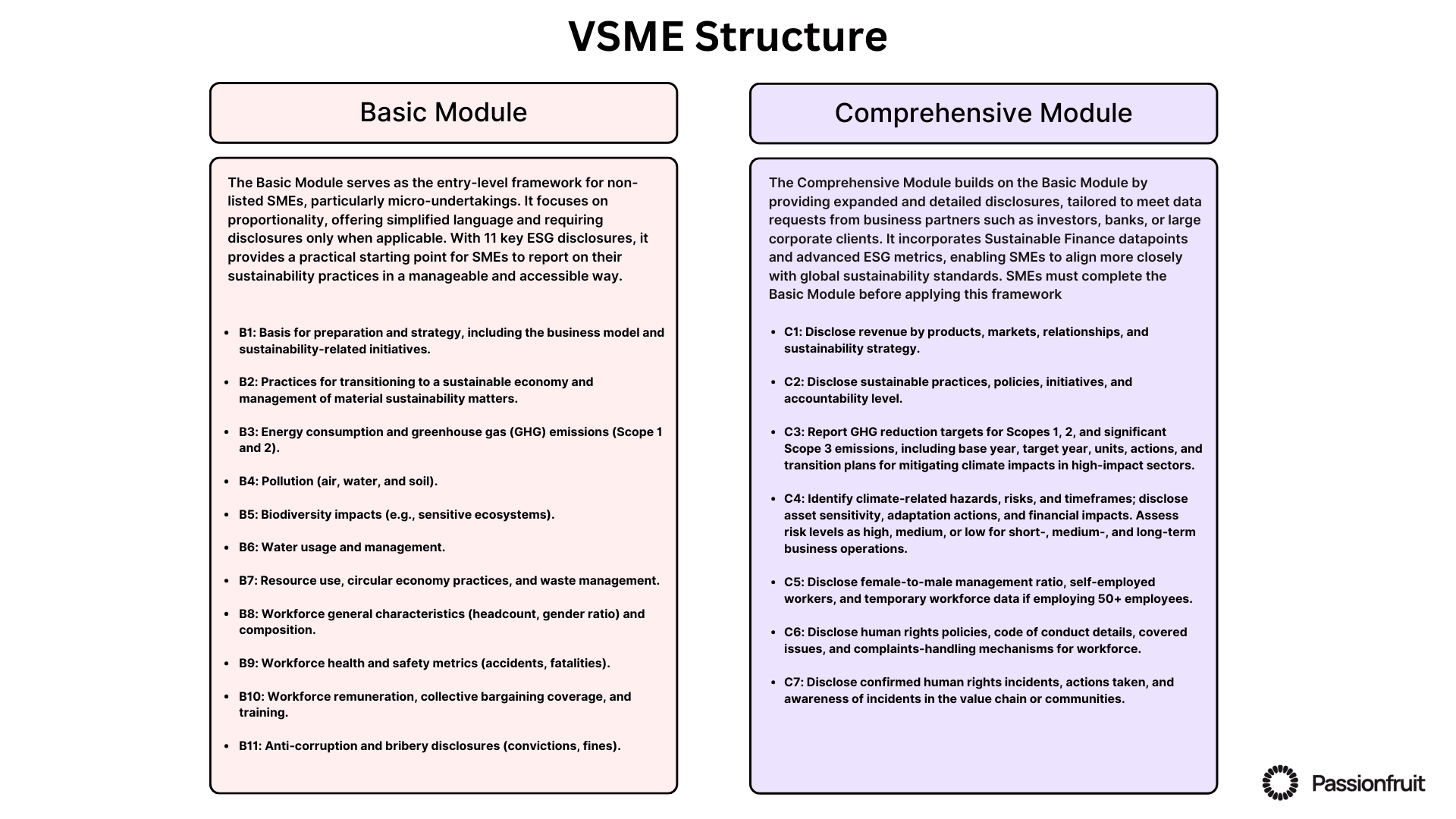

The VSME Standard consists of two modules for preparing sustainability reports: the Basic Module and the Comprehensive Module.

Basic Module

The Basic Module is designed to provide a minimum level of sustainability reporting. It covers a set of key sustainability metrics that all SMEs should be able to report on, regardless of their size or capacity. This module is tailored for micro-undertakings but can also be used by larger SMEs as a starting point. It covers the following categories:

General Information: Basic company details, including the legal form, industry classification, and employee count.

Environmental Metrics: Information on energy consumption, greenhouse gas (GHG) emissions, waste generation, and water usage.

Social Metrics: Reporting on workforce characteristics, health and safety, remuneration, and training.

Governance Metrics: Information on business conduct, including any convictions or fines related to corruption or bribery.

The Basic Module is sufficient for businesses that want to meet the minimum disclosure requirements and gain a basic understanding of their environmental and social impacts.

Comprehensive Module

The Comprehensive Module is intended for businesses that want to go beyond the basic disclosures and provide more detailed information that may be required by banks, investors, or larger corporate clients. It expands on the metrics covered in the Basic Module and includes additional reporting requirements in the following areas:

Business Model and Strategy: A detailed description of the company’s business model and strategy, including any sustainability-related initiatives.

Climate Risks and GHG Emission Reduction Targets: Detailed reporting on the company’s GHG emissions (including Scope 3 emissions) and any reduction targets they have set.

Human Rights: Information on policies and practices related to human rights, including child labor, forced labor, and discrimination.

setting emissions target.

Governance and Diversity: Disclosures on the company’s governance structure, including gender diversity within the governance body and any sectors from which the company derives its revenues.

The Comprehensive Module allows SMEs to provide more in-depth data for investors, banks, and business partners, demonstrating their commitment to sustainability and positioning them as responsible business partners.

Environmental Metrics

One of the key sections in the VSME Standard is environmental reporting. SMEs are required to disclose their impacts on the environment, including their energy consumption, GHG emissions, and pollution levels. Below are the main components:

Energy and Greenhouse Gas (GHG) Emissions

SMEs must report their total energy consumption in MWh, broken down by renewable and non-renewable sources. For example, renewable sources include solar, wind, and hydropower, while non-renewable sources encompass coal, natural gas, and oil. Additionally, they are required to disclose their Scope 1 (direct emissions from owned or controlled sources) and Scope 2 (indirect emissions from purchased energy) GHG emissions. This data is critical for understanding the company’s impact on climate change and setting emissions targets.

Pollution

SMEs must report on any pollutants they emit to the air, water, and soil as part of their operations. Examples of pollutants include particulate matter, sulfur dioxide (SO2), and nitrogen oxides (NOx) for air emissions, as well as chemical discharges into water bodies and heavy metals contaminating soil. Industries such as manufacturing, mining, and agriculture are particularly prone to these emissions. Disclosures should include quantities emitted, mitigation measures undertaken, and compliance with local and international standards to provide a comprehensive view of environmental impact. If the company is already legally required to report such data to authorities, it can refer to the relevant documents or databases. If they voluntarily track their emissions, this data should be included in the sustainability report.

Water and Waste Management

SMEs are required to report their water usage, including total water withdrawal and consumption, especially in water-stressed areas. For example, water-stressed regions like Southern Spain, parts of Italy, or drought-prone areas in Central Europe often face heightened risks of water scarcity. SMEs operating in such regions, particularly in industries like agriculture or manufacturing, should disclose specific water management practices, such as implementing advanced irrigation systems, recycling wastewater, or reducing water-intensive production processes. This ensures responsible resource use while minimizing their environmental impact. Waste management practices are also important, with companies required to disclose the amount of waste generated, as well as their efforts to recycle or reuse materials.

Biodiversity

By incorporating biodiversity into their reporting, SMEs not only demonstrate environmental responsibility but also contribute to global efforts to protect ecosystems and wildlife. Biodiversity reporting involves identifying areas of operation that overlap with protected zones, sensitive ecosystems, or regions of high ecological value. SMEs are encouraged to disclose their impacts on these areas, such as habitat loss, deforestation, or resource depletion. Additionally, businesses can report measures taken to mitigate these impacts, such as habitat restoration, sustainable land management practices, or partnerships with conservation organizations. These disclosures are especially crucial for industries like agriculture, forestry, and mining, which have a significant and direct impact on natural habitats. Including such details not only strengthens transparency but also showcases an SME’s commitment to sustainable practices and global conservation goals.

Social and Governance Metrics

The VSME Standard also requires businesses to report on various social and governance factors:

Workforce

Information on the company’s workforce characteristics must be disclosed, including:

Number of Employees: Total headcount or full-time equivalents.

Gender Distribution: The gender composition of the workforce.

Employee Turnover: The turnover rate for the reporting period, particularly for companies with 50 or more employees.

Health and Safety: Metrics related to work-related accidents, fatalities, and ill health.

Remuneration and Training

SMEs are required to disclose employee remuneration, ensuring that wages meet or exceed the national minimum wage, and report on the percentage of employees covered by collective bargaining agreements. Additionally, companies should disclose the average number of training hours provided per employee.

Governance

Businesses must disclose any convictions or fines for corruption and bribery during the reporting period. Such disclosures are critical for fostering transparency and building trust with stakeholders, including customers, investors, and regulators. By demonstrating accountability and a commitment to ethical practices, businesses can enhance their credibility and strengthen relationships with key partners. This aligns with broader transparency goals, ensuring stakeholders are informed about the company's integrity and compliance with legal and ethical standards. This transparency is crucial for building trust with stakeholders, including investors and customers, and demonstrates a commitment to ethical business practices. This is crucial for maintaining ethical business practices and demonstrating transparency.

Benefits of the VSME Standard for SMEs

By adopting the VSME Standard, SMEs can reap several benefits, including:

Improved Sustainability Management: The VSME Standard helps businesses identify and manage their environmental and social impacts. This can lead to better resource efficiency, cost savings, and a reduced environmental footprint.

Access to Investment: Investors are increasingly looking at sustainability factors when making investment decisions. By providing clear and structured ESG data, SMEs can attract investment and secure financing.

Enhanced Reputation: Transparent ESG reporting helps build trust with customers, suppliers, and other stakeholders. It can also serve as a competitive advantage, demonstrating the company’s commitment to sustainability.

Regulatory Readiness: While the VSME Standard is voluntary, it helps SMEs prepare for future regulatory requirements. As sustainability reporting becomes more mandatory for businesses of all sizes, adopting these practices early will ensure smoother transitions when regulations change.

Market Positioning: By aligning with sustainability goals, SMEs can improve their market positioning, strengthen relationships with customers, and enter new markets where sustainability is a priority.

For instance, a food manufacturer company that adopted energy-efficient practices and reported its reductions in carbon emissions was able to secure contracts with larger eco-conscious corporations seeking sustainable suppliers. Additionally, companies adhering to circular economy principles—such as recycling materials and reducing waste—can appeal to clients in industries like packaging or retail, where sustainable practices are becoming non-negotiable.

The VSME Standard’s guidance on metrics such as renewable energy use and GHG emissions further helps SMEs showcase their efforts. By embedding sustainability into their business models and using the structured framework provided by the VSME, SMEs can highlight their role in the value chain for larger enterprises looking to meet their own regulatory and sustainability commitments. For instance, a small manufacturing company that adopted energy-efficient practices and reported its reductions in carbon emissions was able to secure contracts with larger eco-conscious corporations seeking sustainable suppliers.

Conclusion

The VSME Standard provides SMEs with a practical, scalable approach to sustainability reporting. It offers a flexible framework that allows businesses to disclose key ESG metrics in a way that suits their size and capacity, while also ensuring they meet the growing demand for transparency from investors, customers, and business partners. By adopting the VSME Standard, SMEs can improve their environmental and social performance, attract investment, and contribute to a more sustainable and inclusive economy. As the standard evolves and more businesses adopt it, it will play a critical role in driving the transition to a greener, more sustainable future for all enterprises, big and small.