This guide helps quality officers in the food industry navigate the complexities of CSRD and VSME sustainability reporting frameworks.

Maikel Fontein

7

min

For quality officers in the food industry, keeping up with ever-changing regulations can feel like a constant balancing act. The Corporate Sustainability Reporting Directive (CSRD) and Voluntary Sustainability Reporting Standards for SMEs (VSME) are two major frameworks that shape how companies must report their sustainability efforts. Both frameworks bring different requirements, but understanding them is crucial to staying compliant and competitive.

This guide will break down the core differences between CSRD and VSME, explain how they impact food businesses, and offer clear, actionable steps for navigating these requirements. Whether you’re managing a large corporation or an SME, we’ll help you tackle these regulations without overcomplicating the process, so your team can focus on what matters most: driving sustainability throughout your operations.

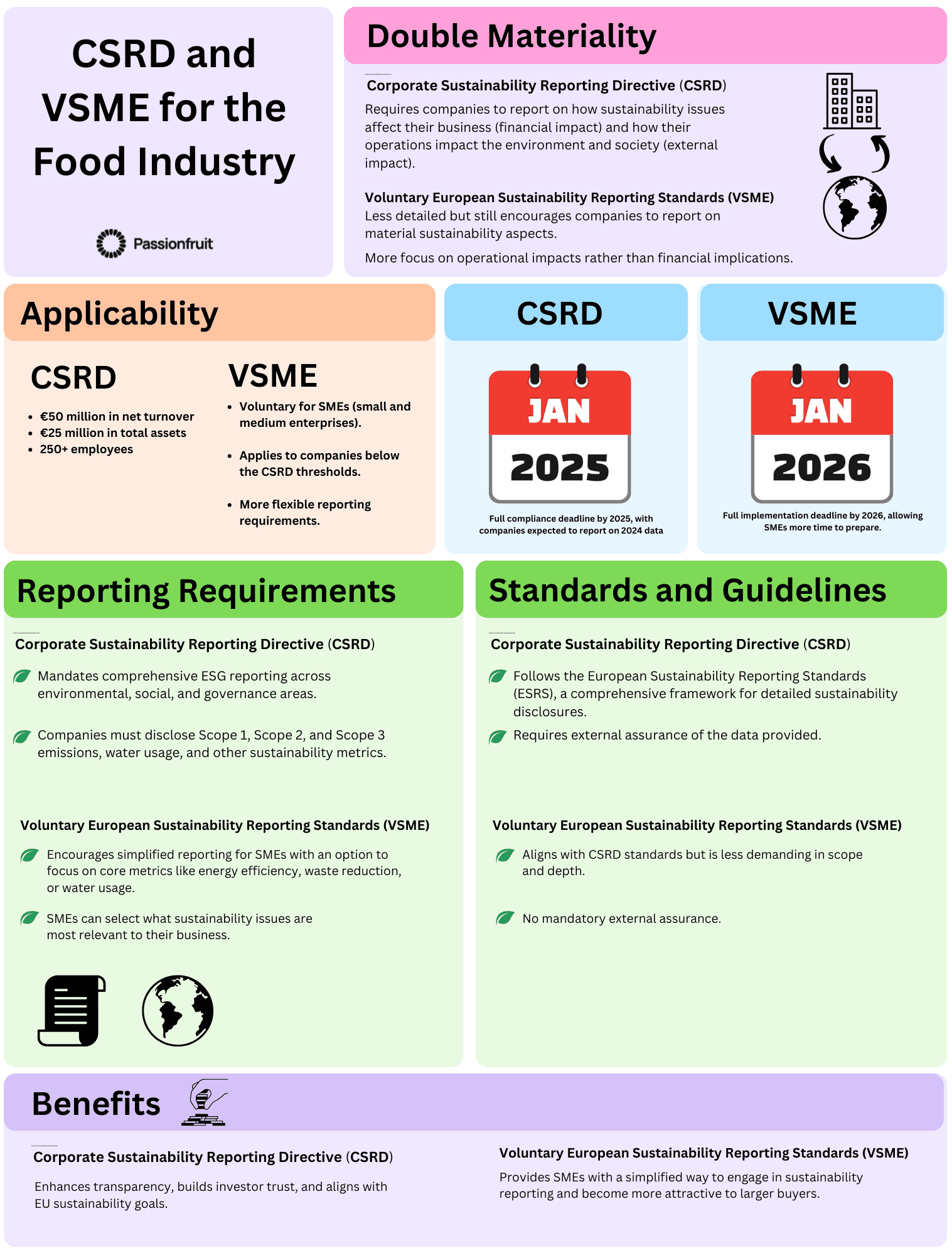

What Are CSRD and VSME?

Corporate Sustainability Reporting Directive (CSRD)

The CSRD, formalized under Directive (EU) 2022/2464, replaces and expands the requirements of the Non-Financial Reporting Directive (NFRD). It mandates the disclosure of information on environmental, social, and governance (ESG) issues, aligning with the EU’s broader sustainability goals, including the European Green Deal and the Paris Agreement.

Key Features of CSRD:

Applicability: All large companies and listed SMEs, excluding micro-enterprises, must comply. Large companies are defined as those meeting at least two of the following criteria:

Net turnover exceeding €50 million

Total assets exceeding €25 million

More than 250 employees

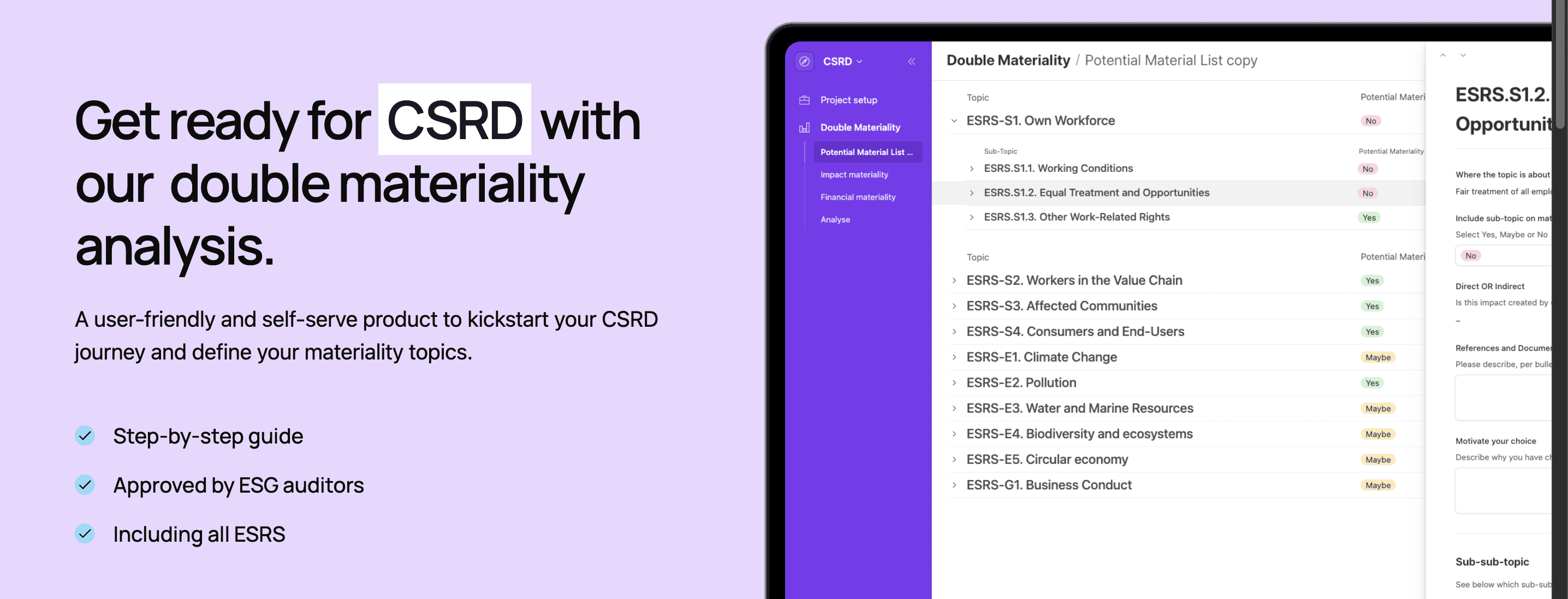

Double Materiality: Companies must report both on how sustainability issues impact their business and how their operations affect society and the environment. According to Article 19a of Directive (EU) 2022/2464, the double materiality concept requires businesses to disclose the impacts of their operations on the environment and society, as well as how sustainability factors affect their financial performance.

Tip: Using Passionfruit double materiality assessment can help you get started on ESG factors that truly matter

Example: A beverage company reports on greenhouse gas emissions from production (impact on society) and how climate risks, such as water shortages, affect its operations.

Standards: The CSRD integrates the European Sustainability Reporting Standards (ESRS) developed by EFRAG to guide the depth and detail required in reporting.

Tip: Familiarize your team with ESRS guidelines through online resources or professional training. Outline specific sector standards, which are vital for companies in food production to ensure alignment.

Audit Requirements: Companies must have their sustainability reports assured by independent third parties. A dairy producer could engage a third-party auditor to validate its GHG emissions data, ensuring it meets CSRD’s reporting requirements and is trustworthy for stakeholders.

Tip: Start building compliance systems early to avoid last-minute challenges. For instance, integrate systems for consistent tracking of environmental data across production facilities so that when the CSRD rolls out, your company is ready.

Why It Matters for the Food Industry:

Food companies are under heightened scrutiny due to their environmental footprint and complex supply chains. The CSRD ensures transparency across issues such as greenhouse gas (GHG) emissions, water usage, and biodiversity impacts—key areas for the sector. The CSRD requires detailed reporting on Scope 1, Scope 2, and relevant Scope 3 emissions. For a food manufacturer, this includes emissions from agricultural inputs, transportation, and packaging. Tracking these emissions from farm to packaging can help ensure accurate and comprehensive reporting by 2025.

Voluntary Sustainability Reporting Standards for SMEs (VSME)

The VSME framework provides simplified reporting standards for SMEs, allowing them to participate in sustainability initiatives without the full administrative burden of CSRD compliance. It emphasizes flexibility and alignment with larger sustainability goals.

Key Features of VSME:

Applicability: This Standard is voluntary. It applies to undertakings 1 whose securities are not admitted to trading on a regulated market in the European Union (not listed). [Article 3 of Directive 2013/34/EU] defines three categories of small- and medium-sized undertakings based on their balance sheet total, their net turnover and their average number of employees during the financial year.

(a) An undertaking is micro if it does not exceed two of the following thresholds:i.

i. €450,000 in balance sheet total;

ii. €900,000 in net turnover;

iii. an average of 10 employees.

b) An undertaking is small if it does not exceed two of the following thresholds:

i. €5 million in balance sheet total;

ii. €10 million in net turnover;

iii. an average of 50 employees.

(c) An undertaking is medium if it does not exceed two of the following thresholds:

i. €25 million in balance sheet total;

ii. €50 million in net turnover;

iii. an average of 250 employees

Flexibility: SMEs can select core metrics relevant to their business operations. The VSME allows companies to choose which sustainability issues to report on based on their size and capacity. A bakery supplier could focus on energy efficiency and waste reduction, critical aspects of their operations, rather than focusing on extensive environmental or social data that may be irrelevant to their scale of operation.

Alignment: Reporting aligns with CSRD standards, enabling seamless integration into larger companies’ compliance efforts. VSME is designed to ensure that smaller companies can participate in sustainability reporting without facing the complex and extensive requirements of the CSRD.

Tip: Use buyer-provided templates to streamline your reporting process. For example, if a food supplier is working with a larger retailer that follows CSRD, they might be given a reporting template for water usage or GHG emissions that aligns with the CSRD framework.

Timeline: Full implementation of VSME standards by January 1st, 2026, allowing SMEs sufficient preparation time.

Tip: Begin gathering data early to identify gaps and adjust processes as needed. Start by tracking core metrics relevant for your businesses. For instance, if you are an dairy supplier, track water usage and animal welfare metrics in preparation for full implementation of VSME.

Why It Matters for SMEs in the Food Industry:

SMEs form the backbone of food supply chains. Adopting VSME standards demonstrates their commitment to sustainability, enhancing their credibility with large buyers and building resilience in competitive markets.

How Quality Officers Can Ensure Compliance

Navigating the regulatory landscape of sustainability reporting requires more than just meeting basic compliance requirements; it’s about integrating sustainability practices into the core of your operations and supply chain. With the CSRD and VSME now in place, quality officers must adapt their processes to ensure both transparency and consistency across all reporting aspects. Let’s break down each critical step to achieving compliance.

Key Areas to Focus On:

Climate Change: Companies must report on their impact related to climate change mitigation and adaptation efforts. This includes setting clear targets for emissions reductions (Scope 1, Scope 2, and Scope 3) and aligning these targets with the EU Green Deal.

Tip: For a large food company, assess GHG emissions across all production and transportation stages. This includes emissions related to agricultural inputs (Scope 3), direct emissions from factory operations (Scope 1), and indirect emissions from energy use (Scope 2).

Water Usage: Water is a critical resource in food production. The ESRS requires detailed reporting on water usage, efficiency improvements, and efforts to reduce water consumption.

Tip: Begin by establishing baseline data on water usage across all production sites, including agricultural processes. Track and report on water waste reduction initiatives, especially if your operations are located in water-stressed regions.

Biodiversity: Food companies must address their impact on biodiversity and ecosystems, including efforts to mitigate deforestation, habitat loss, and ecosystem degradation. This is part of the CSRD, which calls for reporting on environmental risks and opportunities linked to biodiversity.

Tip: If sourcing from regions at high risk of deforestation (e.g., palm oil, soy), consider adopting sustainable sourcing certifications such as the Roundtable on Sustainable Palm Oil (RSPO) or the Rainforest Alliance certification.

VSME: Focus on Core Sustainability Metrics for SMEs

For SMEs, the VSME framework offers a simplified approach. Instead of broad ESG reporting, SMEs are encouraged to focus on core metrics that reflect their direct impact on sustainability. This could include energy efficiency, waste management, or ethical labor practices, with an emphasis on aligning with buyer expectations.

Key Areas to Focus On:

Energy Efficiency: SMEs can track energy consumption across production processes and identify energy-saving opportunities. A small snack producer might focus on energy-efficient machinery or solar panel installations to reduce energy use.

Waste Management: SMEs should focus on waste reduction, recycling efforts, and packaging improvements, particularly in a sector like food production, where packaging waste is a significant concern.

Align your reporting with the expectations of your larger buyers. If your customers are CSRD-compliant companies, they will expect you to report on key areas such as energy use, waste, and water consumption using a simplified version of CSRD guidelines.

2. Engage Suppliers

Supplier engagement is one of the most critical components of achieving compliance with both CSRD and VSME. Under Article 19a of Directive (EU) 2022/2464, companies must provide transparency across their entire value chain, requiring suppliers to report relevant ESG data. This is especially important in the food industry, where supply chains are often long and complex.

Host Workshops to Educate Suppliers

CSRD and VSME both emphasize the importance of engaging suppliers, especially those in key sustainability areas like raw materials sourcing, energy usage, and waste management. Hosting educational workshops or webinars for your suppliers can significantly improve the quality and consistency of the data you receive.

Example: Organize a workshop for agricultural suppliers to explain how reducing fertilizer use impacts GHG emissions. Educating suppliers about these connections can help improve the accuracy of reporting, especially when it comes to Scope 3 emissions, which are often the most challenging to track.

Simplify Processes with Digital Platforms

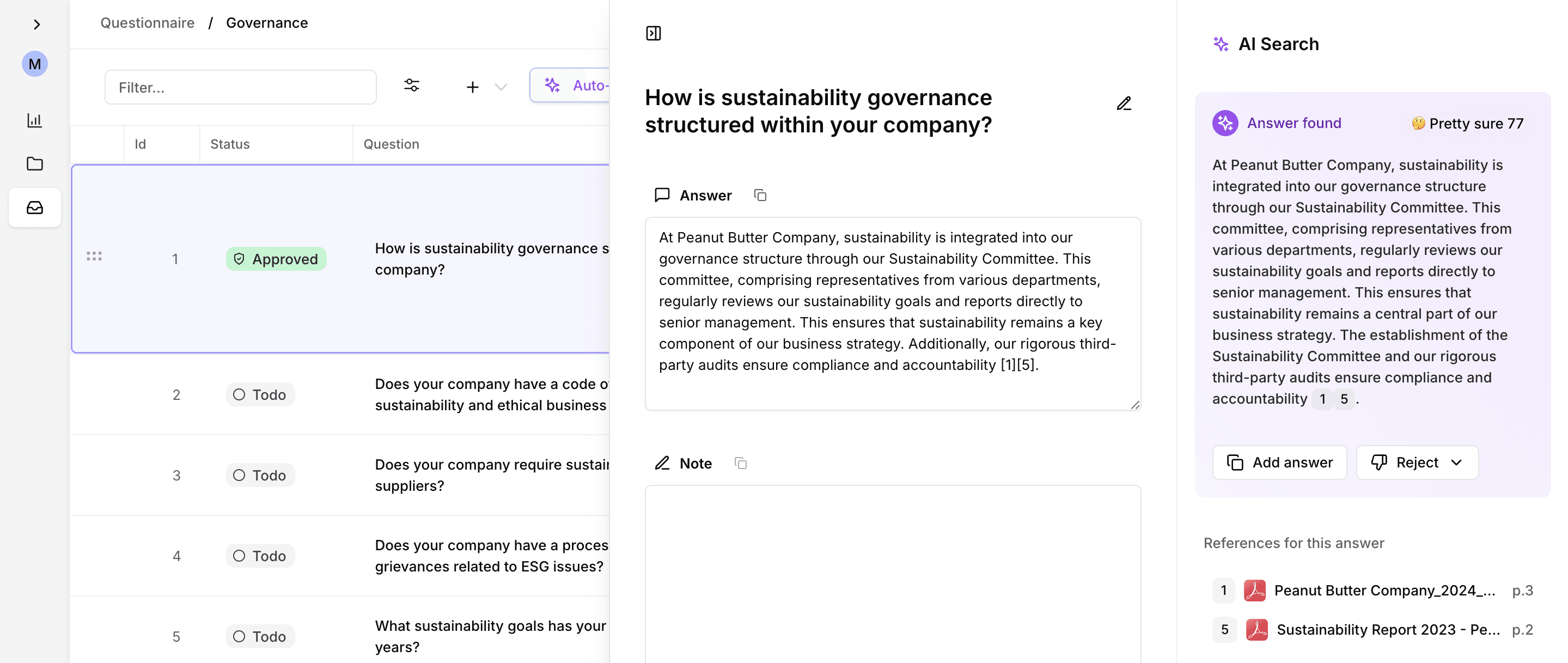

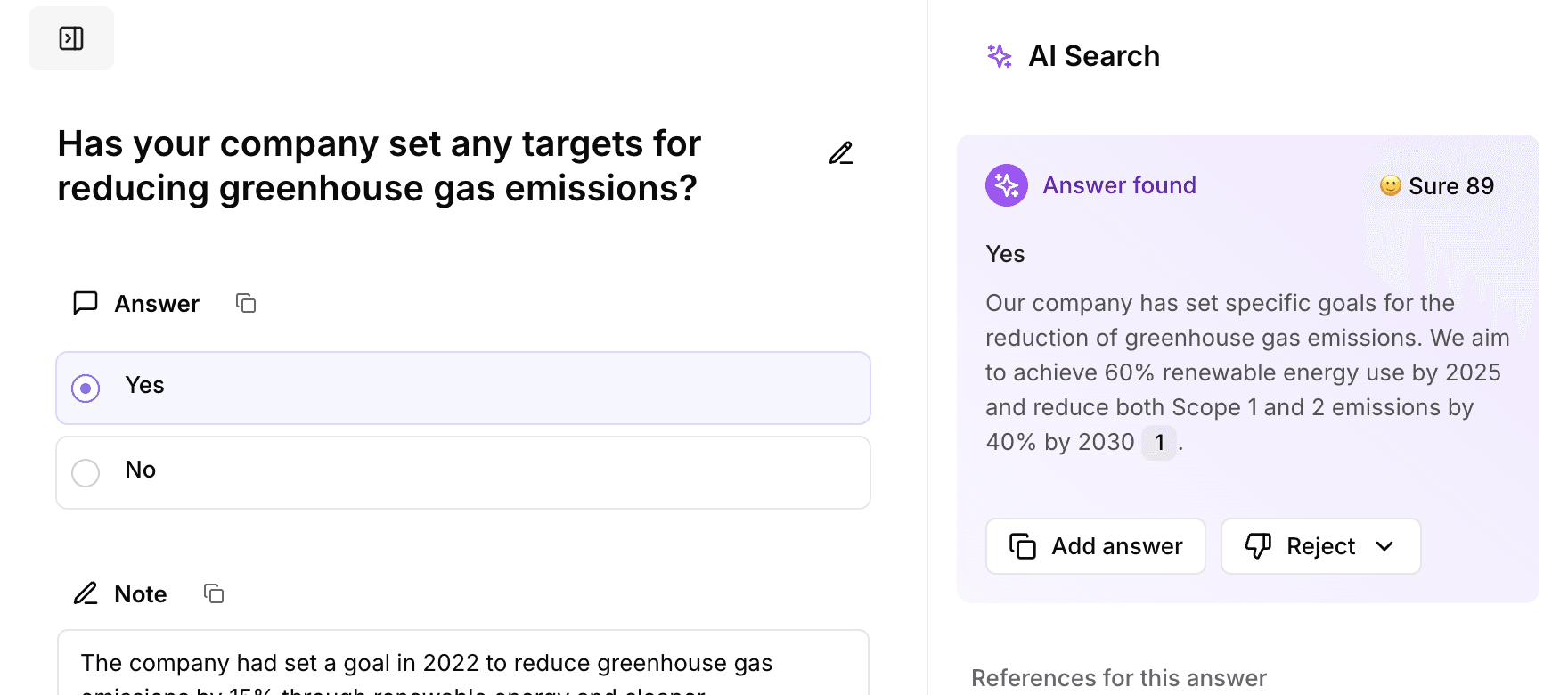

Use platforms like Passionfruit to automate ESG questionnaires and streamline data collection. This reduces manual effort, ensures consistency, and helps suppliers stay on top of reporting requirements. The integration of digital tools can also ensure that suppliers’ data is accurate and updated in real-time.

Example: A large food manufacturer could use a platform like Passionfruit to automatically send ESG questionnaires to suppliers across different regions, capturing data on waste management, energy consumption, and social practices. This ensures that the data is consolidated into one system for easy reporting.

Collaborate on Shared Goals

Collaboration is key to achieving common sustainability targets. Under the CSRD, transparency is crucial, and working with suppliers to improve sustainability practices benefits both parties. Aligning targets with your suppliers, particularly on water usage, energy consumption, and waste management, helps ensure that the entire supply chain is focused on the same goals.

Example: Partner with your suppliers to implement water-saving technologies. Track progress together on reducing water consumption, and use that data in your sustainability reporting.

Leverage Digital Tools

Technology plays a pivotal role in simplifying the complex data collection and reporting requirements of CSRD and VSME.

Passionfruit Platform: Automate ESG Questionnaires

Using a platform like Passionfruit automates ESG, quality, and safety compliance questionnaires, extracting answers directly from a company’s existing data. Serving industries like food & beverage, packaging, manufacturing, and logistics. Passionfruit integrates seamlessly with existing knowledge hubs and supports various formats for questionnaire uploads, all while ensuring robust data privacy and security

Example: By integrating Passionfruit into its operations, a large beverage company can streamline the reporting of water usage across multiple production facilities, automatically compiling data for quarterly or annual sustainability reports.

Assurance Tools: Improve Data Confidence

For both CSRD and VSME, the accuracy of data is essential. Passionfruits confidence score helps users assess the relevance and reliability of the data used in their ESG, quality, and safety compliance reports. This score gives companies a clear indication of how trustworthy the answers are, based on the source and consistency of the data. It provides transparency, allowing users to quickly identify areas that need further verification or improvement. With the Confidence Score, companies can ensure that their sustainability reports are accurate, compliant, and reliable, ultimately building trust with stakeholders and making the reporting process more efficient.

Tip: Passionfruitt offers automated checks and balances to identify gaps in data. These tools highlight areas of improvement, ensuring that companies can correct any inconsistencies before submitting their reports.

Example: A large food company could use Passionfruit to confirm the accuracy of emissions and water usage reports, ensuring that all figures align with CSRD's strict standards for auditing.

4. Adopt a Phased Approach

Both CSRD and VSME offer companies the flexibility to adopt a phased approach to sustainability reporting. This allows businesses to focus on the most critical areas first, building systems and processes as they go along.

Phase 1: Focus on High-Impact Areas (Energy, GHG Emissions)

For large companies, start by tracking high-impact areas, such as energy use and GHG emissions. These are the key metrics that will likely be scrutinized first under CSRD and form the foundation for broader reporting.

Example: Start by tracking electricity usage across your facilities and identifying areas where you can reduce consumption, such as by switching to energy-efficient machinery or installing renewable energy sources. Use these initial data points to set reduction targets.

Phase 2: Expand to Supply Chain and Social Factors

Once Phase 1 is established, begin expanding reporting to include social factors (like labor practices and community impacts) and supply chain issues (such as supplier sustainability practices).

Tip: Use data from Phase 1 to inform and refine your sustainability goals. For example, if energy efficiency is a key target in Phase 1, you may expand this focus to energy-efficient supply chain practices in Phase 2.

Example: A bakery chain can begin by tracking energy consumption and later expand to include metrics on waste management and employee well-being, ensuring a holistic approach to sustainability reporting.

Conclusion

For food companies, ensuring compliance with both CSRD and VSME requires a detailed and phased approach, aligning internal practices and supply chain data with regulatory standards. By integrating sustainability reporting into your operational strategy, using digital tools, educating suppliers, and adopting a phased reporting approach, quality officers can ensure their companies not only comply with regulatory requirements but also become leaders in sustainability within the food industry.

These efforts will drive long-term resilience, improve supplier relationships, and help meet the growing demand for transparency in sustainability reporting, positioning your company for success in an increasingly regulated and eco-conscious market.